I knew the rules.

I had read the books.

I understood Financial Independence.

And I still blew up my finances.

In 2019, I discovered FIRE — Financial Independence, Retire Early — and felt like I had found the secret code to life. I devoured books, podcasts, forums. I graduated nursing school ready to live on 20% of my income and sprint toward freedom.

For a while, it worked.

I house-hacked a duplex. I saved aggressively. I talked like someone who had it figured out.

Then more money arrived — and discipline left.

Travel nursing boosted my income. I financed a Tesla. I told myself I had earned it.

A year later, I quit nursing to buy a business with other people’s money. The numbers were inflated. I wasn’t prepared. I wasn’t the operator I thought I was.

The business collapsed.

The fallout cost me my savings, my duplex, and $280,000 in what I now call “tuition.” It strained relationships and exposed weaknesses I didn’t know I had.

And here’s the uncomfortable truth:

I didn’t fail because I didn’t know the rules.

I failed because I was structurally fragile.

The Real Problem: Fragility

Fragility isn’t ignorance.

It isn’t poverty.

Fragility is:

High fixed obligations

Low reserves

Ego-driven spending

At my worst, I had a $5,000 mortgage, a $700 car payment, collapsing business income, and no meaningful cushion.

One disruption — and everything fell apart.

The math didn’t fail me.

The order did.

The Problem With Modern Financial Advice

Most financial advice assumes stability.

“Max your Roth.”

“Invest early.”

“Buy assets.”

“Use leverage.”

All solid advice — for someone who can absorb risk.

But what about the 28-year-old making good money who is one layoff away from panic?

What about the young couple with rising income and rising fixed expenses?

What about the high earner with zero margin?

The numbers still matter.

But the order of operations matters more.

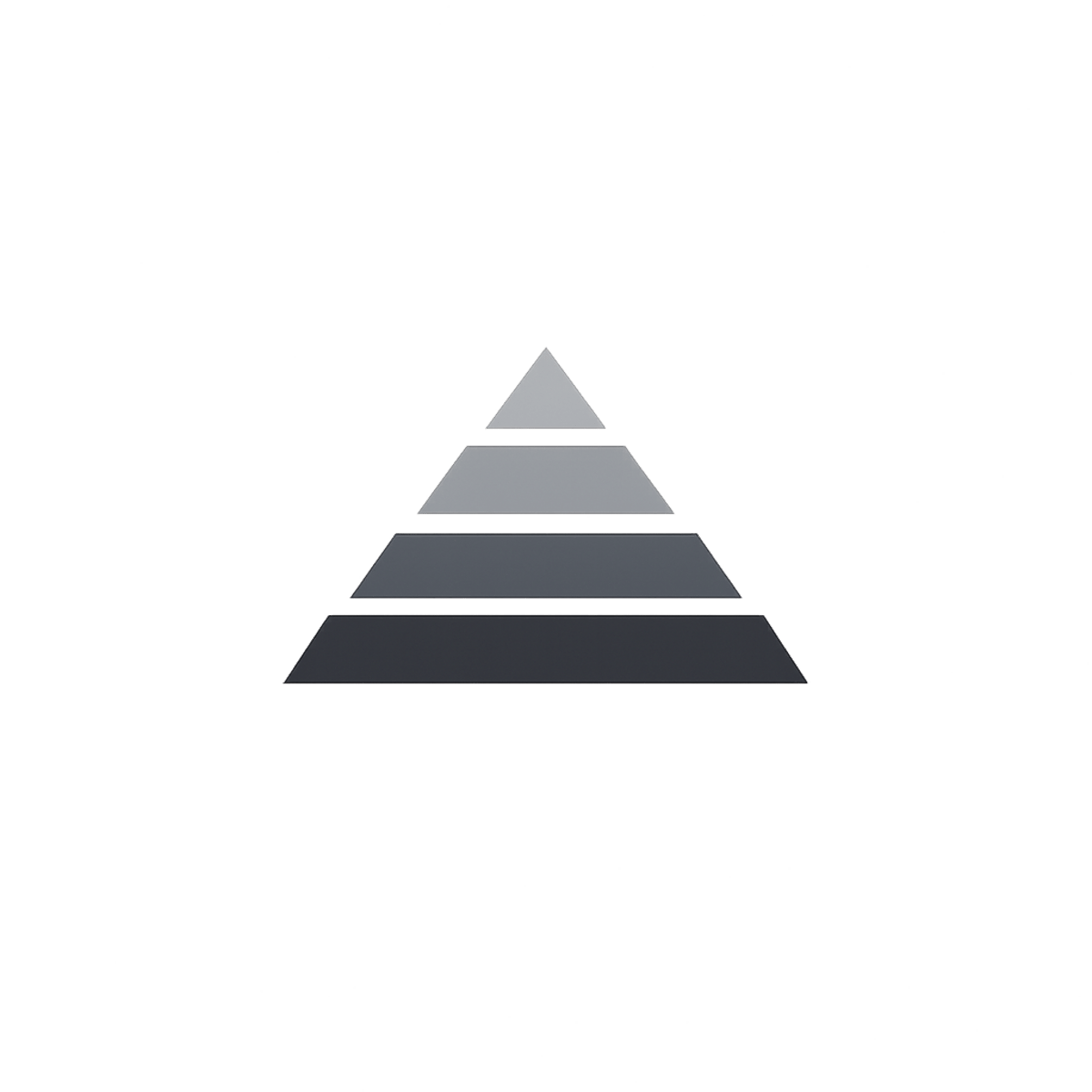

Financial independence is not built in a straight line.

It’s built in layers.

Each layer reduces fragility and increases control.

Stability comes first.

Then margin.

Then leverage.

Only after that does optionality appear.

Most advice skips ahead. It assumes resilience. It assumes you can tolerate risk without consequence.

But if the foundation is fragile, every decision feels heavier than it should.

Before wealth, there must be stability.

Before speed, there must be margin.

The Framework

Phase I: Stabilize

Stop the bleeding.

Cut large fixed expenses.

Build a small emergency reserve.

Eliminate high-interest consumer debt.

Know your real numbers.

Stability is not glamorous.

It’s quiet.

It’s boring.

It’s powerful.

Phase II: Build Margin

Create breathing room.

Expand your emergency fund.

Capture employer matches.

Resist lifestyle inflation.

Margin is what turns emergencies into inconveniences.

Phase III: Create Leverage

Widen the gap between income and obligations.

Increase income aggressively.

Negotiate. Switch roles. Acquire skills.

Make strategic career moves.

Leverage is powerful — but only when it rests on stability and margin.

Phase IV: Optionality

Now you choose your version of freedom.

Max retirement accounts.

Acquire assets.

Start or buy businesses.

Design your ideal lifestyle.

Optionality is not about escaping work.

It’s about escaping fragility.

Where I Am Now

I’m rebuilding from Phase I.

I restarted travel nursing to generate cash flow.

I downgraded the Tesla.

I’m eliminating fixed obligations.

I’m paying down debt before chasing returns.

Cash flow beats ego every time.

I don’t need to retire at 35.

I need to not fear the next bill.

If you make decent money but feel one setback away from collapse, this is for you.

Stability first.

Then freedom.

Subscribe to follow the rebuild.